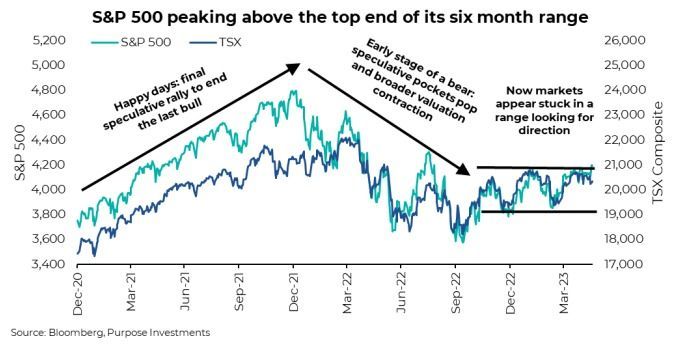

Over much of the past decade, the strategy of buy the dip has become the mantra of many. This was obviously not the ideal strategy for the first nine months of 2022 until the October low. Since then, it has been working once again as the market softened in late December to bounce higher, then weakened in March to bounce higher. To be fair, selling the tip has worked, too, from the mini peaks in November, February and perhaps now…

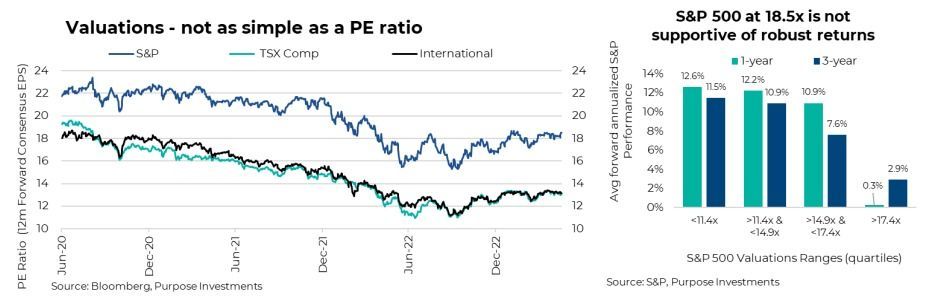

We lean more towards selling the tip – perhaps trimming the tip is more accurate. And we have got valuations on the side. The move higher in the S&P on the back of pretty muted earnings has pushed the forward price-to-earnings ratio up to 18.5. By comparison, it was down to 15 last Fall. This puts S&P 500 valuations well into the most expensive quartile grouping based on data back to the 1950s. And on average, this bucket is followed by pretty muted market returns for the index.

Yields – There is a relationship between equity market valuations and yields available in the bond market. Bonds are a competing asset class, and, everything else being equal, higher yields attract capital. To counter this, equity markets tend to offer lower valuations. Since lower valuations are associated with higher average forward returns, this balances with the higher yield/returns in the bond market.

When yields were below 2%, that was more supportive of higher equity market valuations. Today, with 10-year Treasury yields at 3.7%, we would say this is less supportive of higher equity market valuations. Cash, too, if you can pick up 4-5% with no risk, the expected return in the equity market has to be higher to compensate. Not sure 18.5x for the S&P fits into that framework.

Earnings growth - Price to earnings is a snapshot of valuations, and both the P and E can change. On occasion, when earnings are depressed and/or earnings are expected to grow rapidly, this supports higher valuations. Often the term used is the market will grow into its current valuation. Consensus estimates have the S&P 500 earning about $210 in 2023, which would be a record high. So clearly, earnings are not depressed.

So will earning growth be robust? We are not optimistic. Margins had remained high for many quarters but are now starting to come under pressure. Sales growth is slowing as the economy slows and inflation cools. Meanwhile, costs are still rising from wages to the impact of higher rates. Even if you don’t believe a recession is coming, you probably agree that the economy is set to slow.

Earnings quality - $1 does not equal $1 when it comes to earnings. $1 of earnings from a cyclical company, such as an energy producer or $1 from a levered financial, is not as valuable from the market’s perspective as $1 from a more stable source. Consumer Discretionary earnings are worth less than more stable Consumer Staples. This helps explain the persistent valuation gap between markets such as the TSX and S&P.

On a relative basis, the TSX has a higher weighting in many sectors that simply carry less value per dollar of earnings. And today, a larger portion than average is coming from these same sectors. To show the higher variability of fundamentals, the chart below is the R squared of a number of metrics. If these grew steadily over time, the R squared would be 1, so the further the reading from 1, the more volatile.

Final Thoughts

Even with lower quality of earnings for the TSX and international markets, the valuation gap more than makes up for it compared to the U.S. market. We continue to believe on a relative basis, and we are more comfortable with Canadian dividend-tilted equities or deeper value among international equities such as Europe and Japan.

On a shorter-term basis, maybe we will buy the dip when it comes, but for now, we would rather sell the tip.

— Craig Basinger is the Chief Market Strategist at Purpose Investments

Source: Charts are sourced to Bloomberg L.P. and Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Echelon Wealth Partners Inc. for information purposes only.

This report is authored by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

Disclaimers

Echelon Wealth Partners Inc.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Inc. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional

advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Echelon Partners or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.